I believe that the health of an economy is reflected in the employment growth rate of that economy. When demand for products and services increases, companies hire employees to meet that growing demand. When the reverse happens, companies slow down their hiring and maybe even lay off employees.

I believe that the health of an economy is reflected in the employment growth rate of that economy. When demand for products and services increases, companies hire employees to meet that growing demand. When the reverse happens, companies slow down their hiring and maybe even lay off employees.

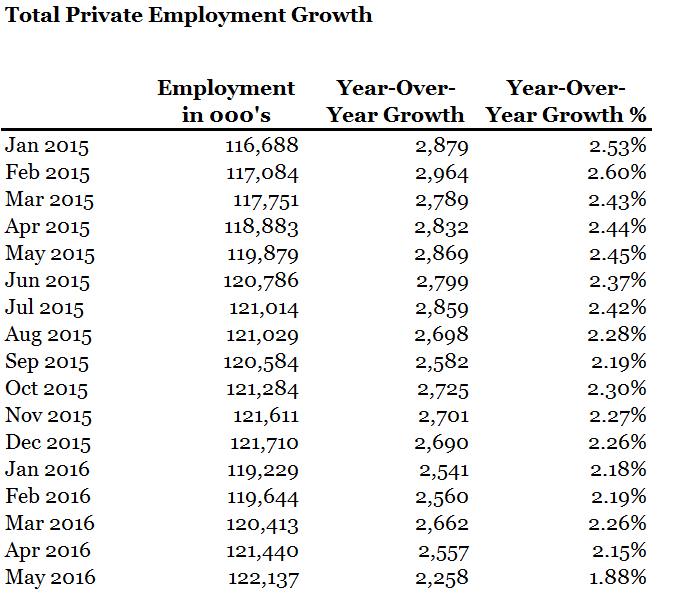

Earlier today, the US Bureau of Labor Statistics released its monthly employment report. Those that follow Financial Slacker, know that I track, analyze, and sometimes comment on this highly anticipated monthly report.

I use this data to gauge where I think the economy is headed. I primarily look at the year-over-year growth percentage each month. And I prefer non-seasonally adjusted total private employment, excluding federal, state, and local government employees. Many in the mainstream media will focus more on unemployment. And although unemployment is important, it is really a measure of capacity not economic growth. Alternatively, private sector employment growth is an indicator of the overall level of current and near-term corporate economic activity.

Employment Growth Lowest Since 2013

For the month of May 2016, non-seasonally adjusted total US private employment was 122.1 million, which is up 2.3 million, or 1.9% year-over-year from May 2015. Month-over-month, May was also up from 121.4 million reported in April 2016.

The good news is that the US continued adding private sector jobs. The bad news is that the US added jobs more slowly than last month. In fact, year-over-year growth in the month of May was the lowest level since March of 2013.

The good news is that the US continued adding private sector jobs. The bad news is that the US added jobs more slowly than last month. In fact, year-over-year growth in the month of May was the lowest level since March of 2013.

If you look at this more recent data, since we emerged into positive growth territory in Aug 2010, we have generally been hovering in the 2% to 2.5% range every month since. We are in one of the longest periods of sustained year-over-year job growth in history.

This month, we saw a drop in the employment growth rate below 2%.

Employment Growth Over the Past 30 Years

For a longer term perspective, if you look back at the data over the past 30 years you can see some very interesting trends.

As I discussed in a prior article, you can clearly see from the chart, over the past 30 years, we have had three periods where total private employment growth was negative:

As I discussed in a prior article, you can clearly see from the chart, over the past 30 years, we have had three periods where total private employment growth was negative:

- 12/90 – 3/92 (16 months)

- 7/01 – 11/03 (29 months)

- 4/08 – 7/10 (28 months)

The first period marked the Gulf War. The second, the attacks on 9/11. And the third, the great housing recession. Although interestingly, the decline in 2001 actually began before 9/11 and dropped below zero in July prior to the attacks. But I’m sure the attacks pushed the declines into record low territory. In 2009, we had three consecutive months of -5.9% year-over-year declines – by far the worst we have seen.

Also over the past 30 years, we have had a number of periods with 3% or better year-over-year growth:

- 10/87 – 4/89 (19 months)

- 3/94 – 6/95 (16 months)

- 3/97 – 5/97, 9/97 – 4/98 (11 out of 14 months)

Unfortunately, we haven’t seen anywhere near 3% growth since then. In fact, after 9/11, we didn’t see 2% growth again until midway through 2005. A growth rate of 2.6% appears to be the new ceiling.

What Should We Expect Going Forward?

History shows that we cannot maintain a sustained high growth level indefinitely. We saw the peak at 2.6% in February last year and have been trending downward ever since.

I don’t want to preach doom and gloom, but based on a number of anecdotal perspectives, I would say we are slipping towards a downturn in the economy. In a recent article, I discussed a number of concerning factors that support this view.

Although still positive, employment growth is trending downward. The stock market started off the year with a significant correction as oil prices plummeted. It has since recovered, but many feel it may be over-valued. Housing prices are again at a peak since the 2008 recession. And we have political instability with the upcoming 2016 Presidential election.

In an environment of uncertainty, it’s worthwhile to consider a few defensive actions such as the following:

- Increase your emergency fund. During a downturn in the economy, having a larger cash allocation than normal isn’t a bad idea. Not only does this give you liquidity if you need it, but it limits losses you may incur in a market correction. I am not suggesting that you begin selling assets, but instead maybe hold-off putting additional money into the market.

- Expand your income sources. Diversified income sources is important in any environment. In a downturn, it’s even more important. Start a side business or two. If you are contemplating leaving your job, take some time to reconsider. Although economic downturns often create opportunities for smaller, more dynamic companies to change directions and make great leaps forward.

- Maintain or even reduce your expenses. If you’re thinking about making a big purchase, be cautious. Now may not be the best time to buy another car. I tend to feel most comfortable minimizing my fixed expenses. Try to keep mortgage payments and other debt payments as low as possible.

- Refinance your mortgage. If you have a fixed rate mortgage, this might be a good time to consider refinancing into an adjustable rate. With property values at their highest level in years and rates at their lowest, you may not ever find a better time to refinance. And if you can reduce your monthly cash outflow, you’ll be in a better position if things get tight.

- Take advantage of underpriced securities. The great thing about a declining market is the buying opportunities it presents. Value investing requires finding companies trading below their intrinsic value. In a rapidly growing economy, finding these opportunities can be difficult. Keep on the lookout for underpriced opportunities in markets that have been negatively impacted.

Obviously I don’t have a crystal ball. Predicting how the economy and how the markets will perform is pretty difficult. And in fact, the US Federal Reserve has indicated they will be raising interest rates over the coming months which is typically an indicator that they feel that the economy is over-heating and they’re worried about inflation. But undertaking the above defensive actions probably won’t hurt even if the economy goes in the other direction.

Readers, do you change your behaviors when you think the economy may be headed in a certain direction? What other actions do you suggest?

[do_widget id=text-8]

{kind=link}

Great ideas to reduce the fallout from an economic downturn there, FS. I think that the way the financially smart amongst us operate is the way man has been doing it since forever.

You reap the harvest when times are good while making provision for future downturns. It seemed to work for thousands of years but now we have credit to bail us out when the going gets tough. Or bankruptcy when the going gets so tough we can’t meet our obligations.

On top of that, there’s social welfare benefits for those who can’t or won’t contribute to their own or anyone else’s harvest.

In times gone past, this would have meant the demise of significant numbers of our population but now it’s all too easy to ignore the past or the current day warning signs and just live for today.

I can’t change what everyone else is doing but can only ensure that my nest stays intact when the bad times hit. Is that a similar philosophy to your own?

That philosophy is similar to mine.

Right now, I’ve started accumulating a larger allocation of cash both to protect against a market downturn, but also because we have significant private school expenses to pay for. We want to make sure those funds are available when needed.

On Friday, I got some stock alerts on my phone and soon figured out it was the first Friday of the month with the non farm payrolls.

Due to my change in job, 1 (increase emergency fund, or in our case: cash for investments) is already started. This should help us to profit from underpriced assets (point 5) when that happens.

We are considering point 3 by haven I car less…

I keep thinking we could get by with only one car for the family (2 drivers). When we need a second one, we could either rent for the day or Uber. Seems like it would be much less expensive.

But I also have two more drivers on the horizon that I’ll be dealing with in a few years.

Your article further strengthens my belief to horde some cash on the side until the market dips. I have been looking for ways to cut my expenses through phone and electricity, it is hard having roommates that don’t care about money. Really hoping to take advantage of the next dip.

Managing expenses is definitely more difficult in a shared environment. When it’s just me, I can live well below my means. But when others are involved, it takes more finesse.

The employment numbers could have been one off. What matters is the 6 months and 12 months trend in my opinion. But there is no doubt the economy has slowed a little probably.

Agree. The trend is really what we should focus on. And that trend has been declining. It’s been such a prolonged period of growth, maintaining that indefinitely is not possible.

It’s hard to make calls on when things will change from good to bad, but it’s definitely impossible to say things will grow forever.

It is getting on near 10 years since the last recession and, hopefully it won’t be anywhere near as bad as 2008, but there will probably be a dip.

At the moment we are saving cash for IVF, nothing to do with the economy. If we weren’t doing that, we would be building up a bigger cash position.

Tristan

Predicting the inflection point is tough. You can see that we’re near the top which means we really have no where to go but down. But the question is when will it go down and by how much?

As a contigent worker in my FT gig, I always believe in having more cash on hand than average. Things in the economy definitely look like there are some wobbles coming ahead. My emergency fund definitely needs to bump up and my cash on hand for purchasing securities needs to bump up so that I can get them at the deal I believe will be happening in the near future.

ZJ:

I’m glad I am not the only one seeing doom and gloom up ahead. Of course, the market has been performing pretty well for the past few weeks.

Hi Financial Slacker,

finally, someone writing something interesting about the current economic condition instead of the usual “How to invest in real estate” or “How to retire earlier” (ops, I just wrote about this one).

I would like to add some of my opinions to the already sound points of this article.

Your observation about the constant deceleration in employment growth coincides with a flat S&P 500 return.

What is it?

As explain in my article “Trading Strategy; How to profit from stock movements” which talk about economic cycles, the US economy is in a “Distribution Phase.”

In this phase, the market stall, move between double and triple up and down as seen in the last August and January.

As FS explained, next is the “Fall-Down Phase”, and you don’t want to be in stocks or long-term bonds.

In the last two weeks, I notice an alarming indicator; any investment classes jumped to the job report news. It means, investors are throwing money at everything has a yield.

It isn’t a professional way to invest money, isn’t it?

FS is giving sound defensive actions above. I would add:

~ If you have a job, keep it. Don’t try to change employment or you might find yourself layoff in the downturn phase.

~ Move some stocks to cash or gold or short-term bonds

~ Pray more often

Happy investing

Thanks Rudy,

Good advice. It’s never fun trying to predict market downturns, but I think it’s prudent to take precautions. You shouldn’t be going all-in either for or against, but subtle changes make sense.